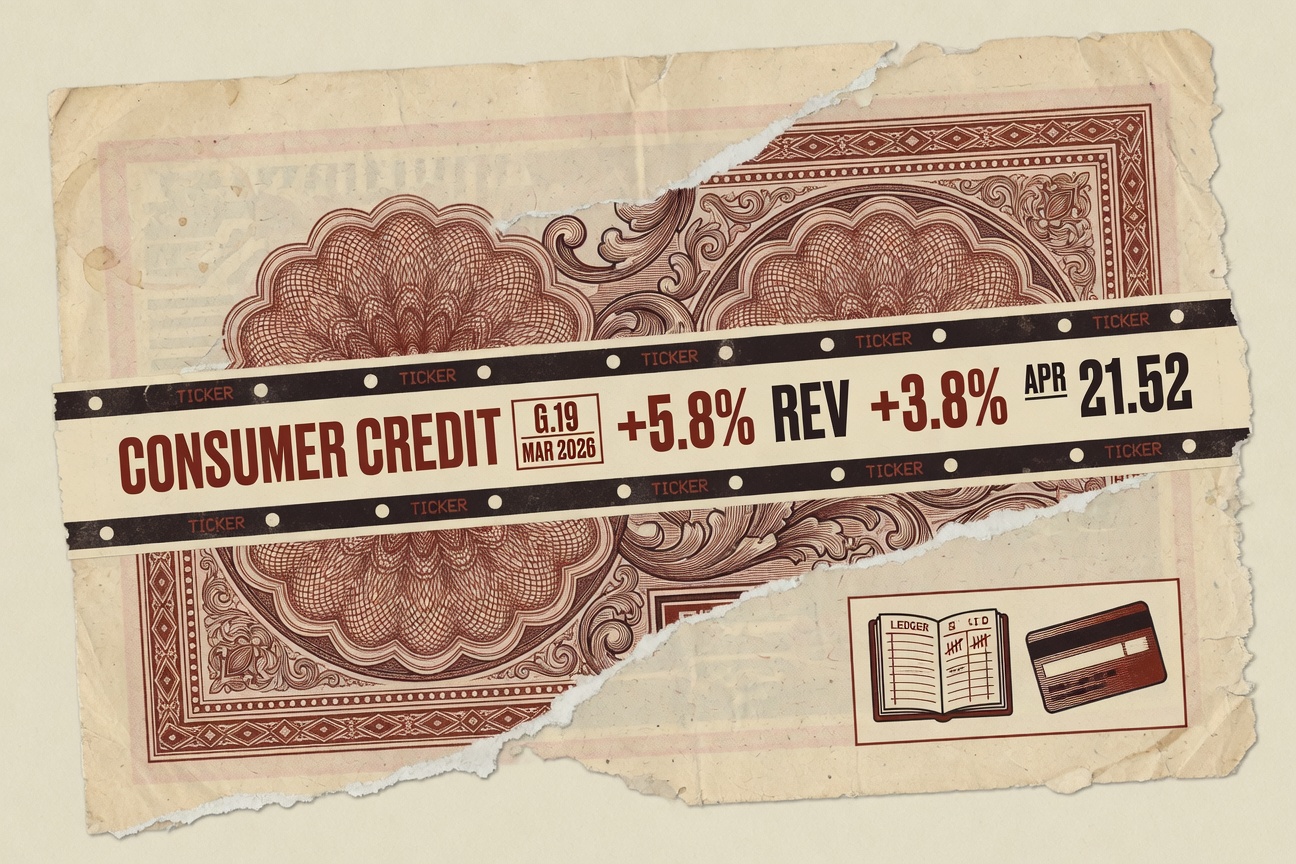

The Federal Reserve reported on Thursday afternoon that consumer credit outstanding rose at a seasonally adjusted annual rate of 5.8 percent in March, the fastest monthly pace since last summer, leaving the total stock at $5.14 trillion. Revolving credit, which is mostly credit card balances, grew at a 3.8 percent annual rate, lifting the revolving total to roughly $1.34 trillion. Nonrevolving credit, which covers auto loans and student loans but excludes mortgages, grew at a 3.0 percent annual rate. The G.19 release is the central bank’s monthly snapshot of how much Americans owe outside of housing, and it is published on the fifth business day of each month at 3 p.m. Eastern.

The headline number is a flow, not a level. A 5.8 percent annual rate means that if March’s pace held for a full year, total consumer credit would expand by about $298 billion. It does not mean balances rose 5.8 percent in March; the actual month-over-month increase was about $25 billion. The distinction matters because it changes how the number reads against the year so far. For the first quarter as a whole, consumer credit grew at a seasonally adjusted annual rate of 3.2 percent. March, in other words, accelerated.

What the breakdown shows

The two subindexes of G.19 do not move the same way for the same reasons. Nonrevolving credit, dominated by closed-end auto and student loan balances, moves with vehicle prices and origination volumes. The 3.0 percent annual pace in March is roughly consistent with the trend of the past two quarters and tracks new auto loan originations reported by the Federal Reserve Bank of New York in its first-quarter Household Debt and Credit data. Revolving credit moves with two things at once: how much consumers charge to cards in a given month, and how much of the prior balance they pay off. A 3.8 percent annual rate for revolving is faster than February but slower than the post-pandemic peaks of 2022 and 2023, when revolving balances grew at double-digit annualized paces for stretches at a time.

Beneath those flows sits a price the release also publishes. In the same G.19 table, the Federal Reserve reports the average annual percentage rate on credit card accounts assessed interest. For the first quarter of 2026, that rate was 21.52 percent. It eased from 22.30 percent in the fourth quarter of 2025 but remains roughly six percentage points above the average that prevailed for most of the 2010s. The interest rate is the cost a household pays for carrying a balance that revolves. At a 21.52 percent APR, an account that carries a $5,000 revolving balance for a year and pays only the interest accrues about $1,076 in finance charges over those twelve months.

What this means for households

Diana Marquez runs a two-chair barbershop in the Mott Haven section of the Bronx and carries about $9,400 across two business cards she opened during a slow stretch in 2023. She pays the minimums most months and a little more in months when foot traffic is good. At her current APR, which she pulled up on her phone at 22.74 percent, the minimum payment retires the balance in roughly nine years if she stops adding to it. She is still adding to it. The store’s clipper supplier raised its wholesale price in March, and Ms. Marquez put the difference on a card.

I know what the rate is. I do not have a cheaper way to keep the shop open this week, so I use the card and I argue with the bill later. — Diana Marquez, barbershop owner, Mott Haven

Hers is one balance behind one of the 192 million credit card accounts the Federal Reserve Bank of New York counted in its first-quarter Household Debt and Credit Report. The New York Fed’s data, drawn from a 5 percent random sample of the Equifax credit panel, put the aggregate credit card balance at $1.25 trillion at the end of March, a figure that is roughly consistent with the G.19 revolving total. The two series do not match exactly because the New York Fed counts balances at quarter-end while G.19 reports monthly averages, and because the New York Fed’s definition of credit card debt is narrower than G.19’s definition of revolving credit, which also includes some non-card revolving lines.

The delinquency line, which has stopped rising

For the past two years, the loudest signal in household credit data was the delinquency rate on credit cards. In the New York Fed’s most recent report, transitions into early delinquency, defined as moving from current to 30 or more days past due, ticked down for credit cards from an annualized 8.7 percent to 8.6 percent. About 2.94 percent of outstanding card balances were at least 30 days delinquent at the end of the first quarter. The aggregate share of all household debt in some stage of delinquency held at 4.8 percent. Those are not pre-pandemic numbers, and they are not improvements anyone would call dramatic. They are the first quarter in roughly two years in which the curve flattened rather than climbing.

Auto loans are a different story. The Federal Reserve’s most recent quarterly Charge-off and Delinquency report put the delinquency rate on auto loans at all commercial banks at 5.2 percent at the end of last year. The New York Fed’s first-quarter data showed transitions into early delinquency on auto loans holding steady at elevated levels. The cohort that has driven that pressure since 2023 is the same one carrying the highest revolving balances: borrowers who bought used vehicles at peak 2021 to 2023 prices and financed them at rates that have not yet rolled off.

What to watch next

The April G.19 reading, which will cover the month in which the Iran conflict pushed retail gasoline prices to their highest levels of the year, is scheduled for release on Monday, June 8. The next New York Fed Household Debt and Credit Report, which adds delinquency-transition detail by age cohort and ZIP code-level distress, is scheduled for August. The Federal Open Market Committee, which held the federal funds target range at 4.25 to 4.50 percent at its May 14 meeting last year, next meets on June 17, with a Summary of Economic Projections that includes the committee members’ central tendency for the funds rate at year-end. The dot plot from the March meeting had a median of one quarter-point cut in 2026.

For households carrying revolving balances, the FOMC path is the variable that determines whether the 21.52 percent average APR drifts lower over the next two quarters or sticks. Credit card APRs reset off the prime rate, which moves with the Fed’s target range. A single 25 basis point cut, if the Fed delivers one in 2026, would lower the average card APR by roughly the same amount over the following billing cycles. On a $5,000 balance, that is about $13 a year. Ms. Marquez did the arithmetic on her phone, looked up, and said it would buy her a sandwich.