Nvidia reported revenue of $81.6 billion for the quarter ended April 26, 2026, the company said in a Form 8-K filed with the Securities and Exchange Commission on Wednesday, May 20. That figure is up 20 percent from the prior quarter and up 85 percent from a year earlier, and it landed roughly $2.5 billion above the $79.2 billion Wall Street consensus going into the release. Data Center revenue alone was $75.2 billion, larger than the company’s entire revenue of $44.1 billion in the same quarter a year ago. The company also disclosed that no shipments of Data Center Hopper products to China occurred during the quarter, against $4.6 billion in the same quarter of fiscal 2026, and stated in its outlook that it is "not assuming any Data Center compute revenue from China" for the second quarter. The Board separately approved an additional $80.0 billion to the share-repurchase authorization and raised the quarterly cash dividend from $0.01 to $0.25 per share. The stock fell 0.9 percent in the next trading session.

The headline number is large enough that the unit deserves a sentence of its own. $81.6 billion is total revenue for a single 13-week period, not an annual figure. Annualized at the same pace and gross margin, the company is on a run-rate close to $326 billion in revenue and around $215 billion in non-GAAP operating income. Those run-rate figures are arithmetic, not guidance (the company guided only one quarter forward), but they put the scale of the quarter in a frame that fits next to the rest of the index. Apple’s total revenue for the comparable fiscal quarter ran around $95 billion; Microsoft’s ran around $70 billion. Nvidia did not exist in this revenue tier two years ago.

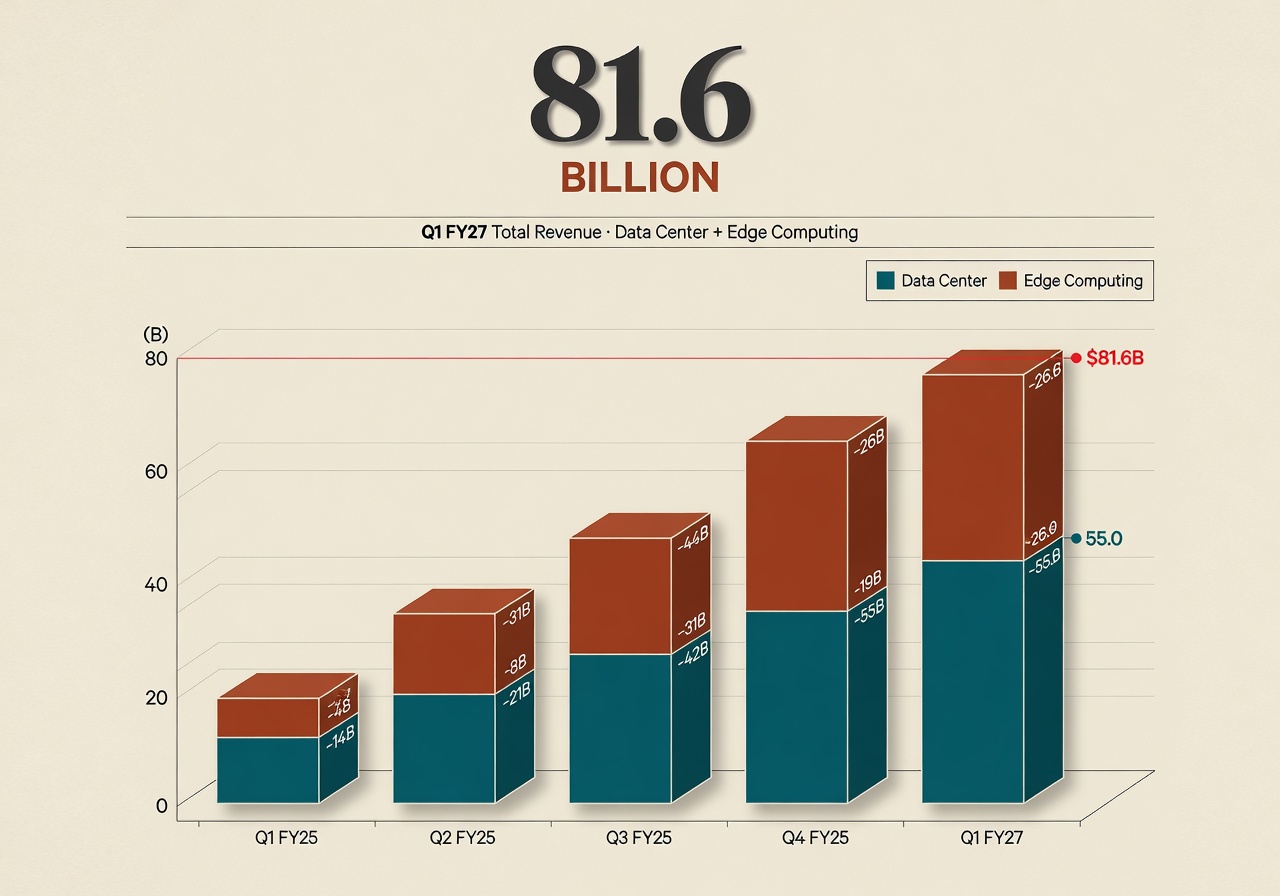

Where the revenue came from

Nvidia is transitioning its reporting framework this quarter from product-family sub-segments (compute, networking, gaming, professional visualization, automotive) to two market platforms, Data Center and Edge Computing, with Data Center further split into Hyperscale and ACIE (AI Clouds, Industrial, and Enterprise). Under the new framework, Data Center revenue was $75.2 billion, up 92 percent from a year ago and up 21 percent sequentially. Hyperscale, which captures the public clouds and the largest consumer internet companies, was $37.9 billion, up 115 percent from a year ago. ACIE, which captures AI clouds, sovereign customers, and industrial and enterprise buyers, was $37.4 billion, up 74 percent from a year ago. The two sub-markets are now roughly equal in size. Edge Computing, which captures PCs, workstations, game consoles, AI-RAN base stations, robotics, and automotive, was $6.4 billion, up 29 percent from a year ago. Under the old framework, which the company published in parallel one last time, Data Center compute was a record $60.4 billion and Data Center networking was a record $14.8 billion, up 199 percent year over year on the strength of InfiniBand, Spectrum-X Ethernet, and NVLink sales attached to the Blackwell 300 ramp.

The composition matters because it shows where Nvidia’s revenue diversification stands today. A year ago, the hyperscalers were a clear majority of Data Center revenue. This quarter, the company says Hyperscale "remained at approximately 50 percent of Data Center revenue, while the remaining 50 percent came from a continued diversification of customers, including AI Clouds, industrial, enterprise, and sovereign customers." The "sovereign" qualifier is doing work in that sentence. Nvidia has been disclosing for several quarters that nation-states and national-champion buyers are part of the customer mix; this quarter, that channel sits inside a $37 billion line.

The China line

No shipments of Data Center Hopper products to China occurred during the quarter, compared with $4.6 billion in the first quarter of fiscal year 2026. — Nvidia CFO Commentary on First Quarter Fiscal 2027 Results, filed with the SEC on May 20, 2026

The cleanest statement in the filing is the one about China. In the first quarter of fiscal 2026, the same period a year earlier, when current U.S. export controls on advanced AI accelerators were still being phased in, Nvidia shipped $4.6 billion of Data Center Hopper products into China. In the first quarter of fiscal 2027, that figure was zero. The outlook line is just as direct: the company "is not assuming any Data Center compute revenue from China" in its $91.0 billion plus-or-minus-2-percent guide for the second quarter. That assumption is consistent with the U.S. Department of Commerce export controls announced through Bureau of Industry and Security rulemaking in 2024 and 2025, which restrict the export of advanced computing chips, including Nvidia’s H20 variant, to China and a list of other destinations. The $4.5 billion H20 inventory and purchase-obligation charge that compressed gross margin in the first quarter of fiscal 2026 is the reason this quarter’s GAAP gross margin of 74.9 percent reads 14.4 percentage points higher than the year-ago 60.5 percent. Take out the China line and last year’s margin would have been considerably closer to this year’s. Take it out of this year and there is nothing else to take out: the line is already zero.

For a household reader, the China line matters in a specific way. The 0.9 percent drop in the share price the following session reflects a market that had largely priced in the absence of China. It is, in trader shorthand, the headline that did not move the stock, and the absence of movement is the disclosure’s confirmation that the market expected what the company described.

Why GAAP net income was $58.3 billion and non-GAAP was $45.5 billion

The two earnings numbers Nvidia publishes diverged sharply this quarter, and the difference is worth a sentence because it is the kind of disclosure that gets repeated incorrectly. GAAP net income was $58.3 billion, up 211 percent from a year ago, and GAAP diluted earnings per share were $2.39, up 214 percent. Non-GAAP net income was $45.5 billion, up 139 percent, and non-GAAP diluted earnings per share were $1.87, up 140 percent. The single largest line that explains the gap is $15.9 billion of net gains from equity securities, which the company describes as "driven by unrealized gains in publicly-held and non-marketable equity securities." Those gains hit GAAP net income immediately but are excluded from the non-GAAP measure, because they are paper gains on Nvidia’s strategic stakes in other companies rather than operating income from selling chips. Operating income, which is the cleaner read of the chip business, was $53.5 billion on a GAAP basis and $53.8 billion on a non-GAAP basis. Those two figures are within roughly half a percent of one another, and they are the right two numbers to compare quarter to quarter when the equity-portfolio mark fluctuates.

What the dividend hike and the buyback signal

Nvidia raised the quarterly dividend from $0.01 to $0.25 per share, a 25-fold increase, payable on June 26, 2026, to shareholders of record on June 4. At the new rate, the annualized dividend is $1.00 per share against a share price that closed at $235.74 at its all-time high on May 14, the week before the report, a forward yield of roughly 0.42 percent. The dividend is not the cash-return story; the buyback is. The company returned approximately $20.0 billion to shareholders through share repurchases and cash dividends during the quarter, and the Board authorized an additional $80.0 billion to the repurchase program on May 18, on top of $38.5 billion remaining at quarter-end. At the current pace of repurchase, $118.5 billion of authorized buyback is more than five quarters of capacity, without an expiration date. Cash, cash equivalents, and marketable debt securities were $50.3 billion at quarter-end, and operating cash flow for the quarter was $50.3 billion, up from $36.2 billion in the prior quarter. Inventory was $25.8 billion, up from $21.4 billion sequentially, and total supply-related commitments were $119.0 billion. The company is, in plain terms, simultaneously running the largest semiconductor build-out in the industry’s history and the largest capital-return program in its own.

What the Q2 guide says and does not say

The outlook for the second quarter of fiscal 2027 is $91.0 billion in revenue, plus or minus 2 percent. That midpoint implies sequential growth of roughly 11.5 percent and year-over-year growth of roughly 53 percent. GAAP gross margin is expected at 74.9 percent and non-GAAP at 75.0 percent, both with a 50-basis-point band. GAAP operating expenses are expected at approximately $8.5 billion and non-GAAP at approximately $8.3 billion, both up roughly $0.9 billion from the quarter just reported, an indication that Nvidia is continuing to scale headcount, compute, and engineering investment. The full-year tax-rate range is 16.0 to 18.0 percent. The guide assumes zero Data Center compute revenue from China, a clean assumption to model against even if the actual outcome turns out to be a small positive number. Two factors are not in the guide. The first is what happens to the Blackwell 300 ramp curve in the second half. The second is the demand response from sovereign and ACIE buyers to the announcement that Nvidia is treating their revenue as the structural growth engine rather than the upside option. Neither is a forecastable number; both will be visible in the August release.

What it means for a household

For a household with a 401(k) holding an S&P 500 index fund, Nvidia is now roughly 7 percent of the index by market capitalization, the largest single-name weight. A quarter like this moves the value of that fund less than the 0.9 percent next-day stock reaction suggests, because the index is also weighted by the rest of the AI capex chain (Microsoft, Alphabet, Amazon, Meta, Broadcom, Oracle), and those names move on related news. For a worker employed at a hyperscale data-center build site, the $119.0 billion of supply-related commitments and the $30.0 billion of multi-year cloud service commitments described in the CFO commentary are the demand-pull side of the construction labor market for the next several quarters. For a household watching the AI debate from outside the financial market, the relevant figure is the gap between the company’s reported scale of customer diversification and the absence of a corresponding employment number disclosed in the release. Nvidia is again the most consequential single quarter of corporate earnings in the index; the disclosure framework around what that scale means for workers, customers, and competing economies continues to lag the disclosure framework around what it means for shareholders.