The story of the year in media is being told in dollars. A $111 billion deal. A $6.2 billion local-broadcast roll-up. Investor calls, regulatory hurdles, and a Texas billionaire’s son explaining $6 billion in promised cost savings to analysts. All of that is the part you can put in a chart. The part you cannot put in a chart is the part that will reach the most people. Sometime after the Paramount and Warner Bros. Discovery merger closes, a viewer is going to open one app and find a recommendation rail that has quietly been rewritten.

On March 2, on an investor call about the combined Paramount Skydance and Warner Bros. Discovery, the new chief executive David Ellison said the plan was to combine HBO Max and Paramount+ into a single direct-to-consumer service. The unified product, Ellison said, would have a little over 200 million subscribers worldwide. Variety, the Hollywood trade that covered the call most closely, treated the line as a punctuation mark inside the larger M&A story. It is not a punctuation mark. It is the entire sentence, for most of the people who will be affected.

Two libraries are about to sit on one homescreen. On one side: the catalog that built the modern prestige drama, from The Sopranos through Succession, plus a documentary unit and Last Week Tonight. On the other: the catalog that runs a parallel American culture, from a sixty-year-old Star Trek franchise to Yellowstone spinoffs to the SpongeBob universe to Nickelodeon and MTV libraries that shaped two generations of children. The companies have positioned the combination as an addition. In practice, every consolidation also performs subtractions.

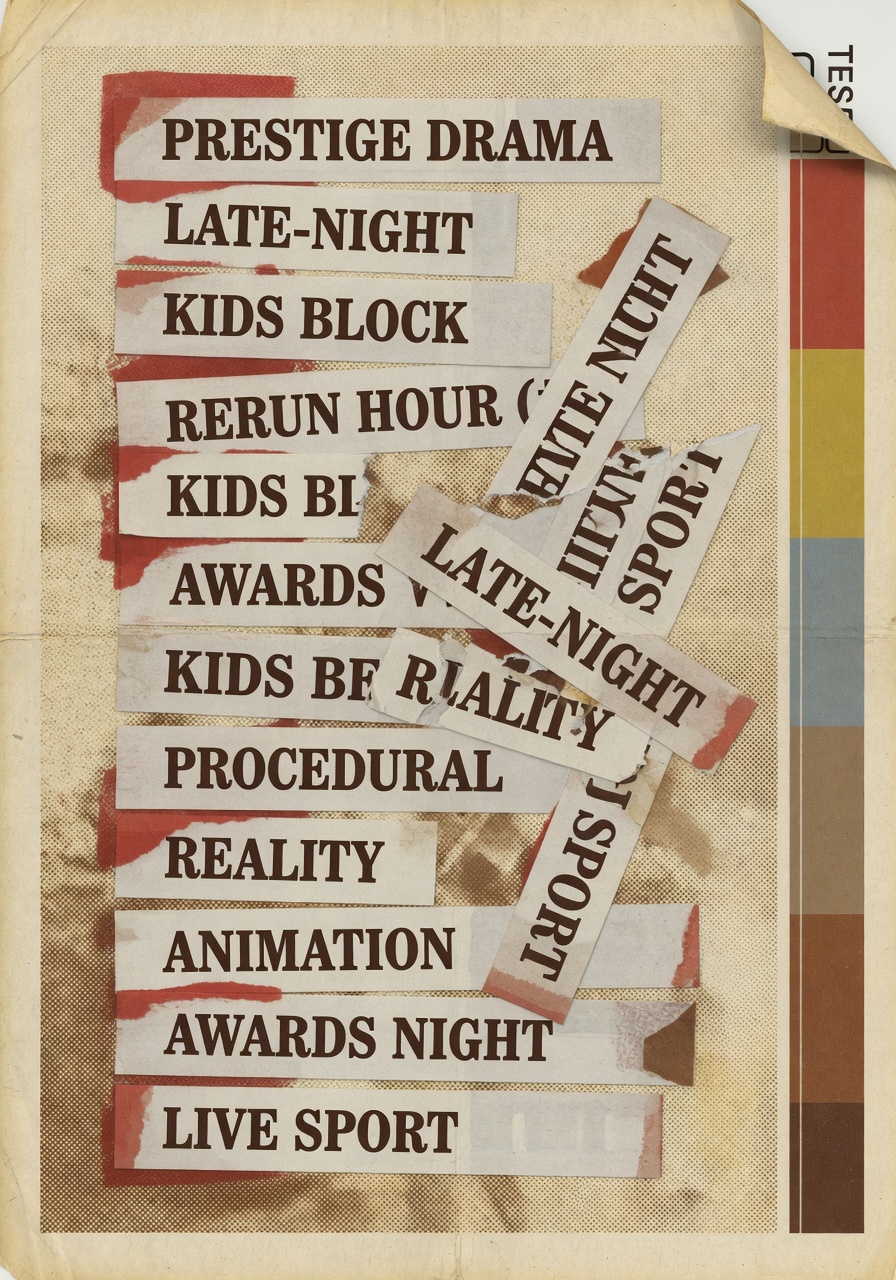

The shelf is the editorial decision

The most consequential editorial decision a streaming service makes is not what it commissions. It is what it places on the first scrollable row when an app opens. Industry consultants have been measuring this for several years. AlixPartners, in its 2025 Media and Entertainment Predictions, wrote that the streaming sector had grown to more than 200 platforms and that 42 percent of subscribers were “serial churners,” cycling on and off services as the recommendation rails failed them. The number is striking on its own. It is more striking when you sit with what it implies, which is that the dominant form of audience behavior on streaming is dissatisfaction.

Inside that dissatisfaction, what people seem to be reaching for is not more content. It is a service that knows what it is for. The Disney bundle was the first product to admit this out loud, by stapling Hulu and Disney+ together so the family-and-prestige split could be reconciled at the homescreen. The combined HBO Max and Paramount+ service is a much larger version of the same bet, and a much harder one, because the two libraries do not share an identity the way the Disney properties do.

The most important editorial decision a streaming service makes is not what it commissions. It is what it places on the first scrollable row when the app opens. — The Moxley Press

A person who came up on HBO and a person who came up on Paramount+ are not, culturally speaking, the same viewer. The HBO viewer was trained on appointment television, ten-episode seasons, and a network identity that announced itself in the opening static. The Paramount+ viewer was trained on the long-tail catalog: a Star Trek series running across decades, a library of procedurals, the cable-childhood archive of Nickelodeon. Both viewers will be looking at the same first row, ranked by the same algorithm, tuned to the same business goal of reducing churn.

What “duplicate” quietly means

Inside the operational work of combining two streaming catalogs, there is a category that does not yet have a public name. Internally, large platforms call it deduplication or rationalization. It is the process by which a combined product decides what to keep visible, what to make searchable but not surface, and what to retire from the carousel entirely. Two reality competition shows in the same niche will not both get a tile. A documentary on the same subject from each library will not both get pushed. Two long-running animated procedurals about the same kind of family will compete for the same slot.

The companies will say, accurately, that the retired titles are still in the catalog. They will be findable by search. This is true. It is also true that the share of viewing accounted for by search, on any major streaming service, is small. Discovery happens on the rail. What is not on the rail is, for most users, not in the library.

Nielsen’s monthly Gauge report, the closest thing the industry has to a public scoreboard, captured the trend in numbers. In December 2025, streaming reached 47.5 percent of total television viewing, the largest share the Gauge has ever recorded. Paramount Streaming on its own reached 2.5 percent of all TV usage, driven heavily by one show, the Taylor Sheridan series Landman, and by NFL games. That is the texture of how a streaming service actually performs: a small number of tentpoles do enormous numbers, and the rest of the catalog runs as background. A bundle does not change the math. It changes which tentpoles get the front-row tiles.

The middle is the thing being lost

The category of programming most exposed to this transition is the one that has the hardest time defending itself: the cultural middle. Not the prestige limited series with the awards campaign. Not the franchise tentpole with the merchandise pipeline. The category in between. The well-made one-season experiment. The mid-budget romantic comedy. The documentary that did not break out but found its audience over years. The animated show whose fans skew older than its marketing assumed. All of these earn their slot today partly through institutional momentum inside their home service. Inside a bundle that has to justify its own thumbnail real estate, they get harder to defend.

The cultural argument for the combined service is that scale enables ambition. That is plausibly true at the top of the catalog. It is less obviously true at the middle. The middle is where most of the work that builds a culture actually lives, and the middle is the part of the catalog that consolidation tends to thin.

Why the local-TV story matters here

A second consolidation closed in March, and it sits inside this same cultural-supply story. Nexstar Media Group closed its $6.2 billion acquisition of Tegna on March 19, after a Federal Communications Commission waiver of the long-standing 39 percent national ownership cap. The combined company owns 265 television stations across 44 states, an antitrust posture that two federal lawsuits are still actively challenging. The deal is the largest local-broadcast roll-up in recent memory. The streaming bundle is the most visible piece of the consolidation wave, and the local-broadcast roll-up is the structural piece, but they are answering the same question from opposite ends. Who gets to decide what 200 million people see when they open an app, or turn on a local newscast, this week?

The standard frame for those decisions used to be regulatory. There were rules about ownership caps and competition. The rules are still on the books. The pace at which they are being waived, or worked around, is the pace at which the question is being privatized. A handful of companies, plus their recommendation algorithms, plus their consolidated ad-sales teams, get to make calls that used to require permission. The streaming bundle is the consumer-facing edge of that shift. The recommendation rail is where you see it first.

What to watch next

There are three signals worth tracking once the combined service launches. First, the public press releases about which originals from each library are getting greenlit or renewed. The library that gets the renewals tells you which side of the merger is winning the identity argument. Second, the published recommendation taxonomies, which surface in the help-center pages and the API documentation that third-party developers see. Those taxonomies are the closest thing to a written editorial policy a streaming service produces. Third, the churn numbers in the first four quarters after the bundle goes live. Subscription fatigue is the dominant consumer story of this decade in media. If the bundle does not make a noticeable dent, the consolidation argument loses its consumer-facing rationale, and the case will have to be made on cost savings alone.

For now, the deal is still pending its third-quarter close, and the regulatory questions, both in the United States and in the European Union, are real. But the strategic argument has been made in public, and the homescreen will follow. Two libraries that built two distinct American televisual cultures are about to share a first row. Whoever decides what sits on it will be making one of the larger editorial decisions of the year, on behalf of an audience that, in the deal documents, is described in subscriber counts.